Sophia’s Thoughts On Token Models Under Pressure

A wave of crypto project shutdowns in 2026 is exposing something the bull market obscured: many token models were never built to survive stress. The question is not which projects ran out of luck, but which ones were structurally fragile from the start.

These are Sophia's Thoughts:

A cluster of crypto project failures in 2026, including Dmail, Tally, Step Finance, and BlockFills, reflects not market misfortune but a deeper structural breakdown in how token-based funding models handle real operational pressure, particularly when tokens serve simultaneously as product utility, community incentive, and financing instrument.

Tokens designed to function as both product and financing mechanism create a fragile alignment between operators, holders, and users that, as restructuring advisor Roshan Dharia notes, collapses precisely when it is needed most, leaving no structured path to recapitalization.

As regulatory scrutiny on AML compliance intensifies across multiple jurisdictions simultaneously, projects with weak token utility and fragmented stakeholder structures face an increasingly narrow path to recovery rather than an orderly wind-down.

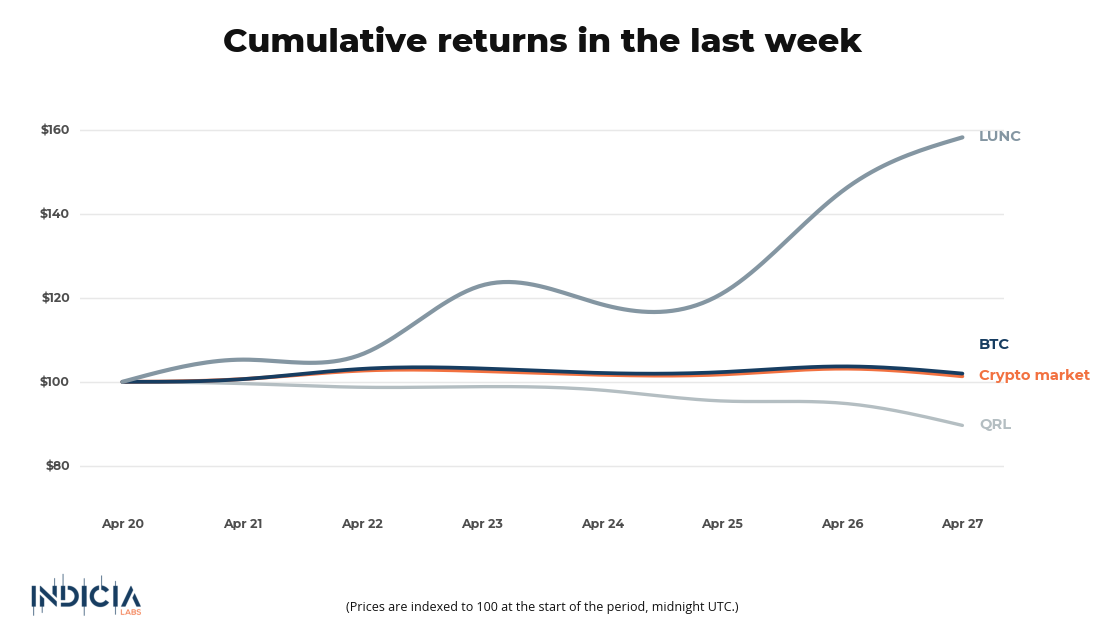

🚀 Last week’s market performance

The broader crypto market gained 1.3% over the past seven days, with Bitcoin (BTC) up 2.0% as sentiment held broadly steady. Terra Luna Classic (LUNC) was the standout performer, surging 58.2% on a renewed wave of speculative activity. Quantum Resistant Ledger (QRL) was the week's worst performer, declining 10.4%.

🧐 What is your crypto mood today?

In each Sophia's Thoughts newsletter, we ask about your crypto mood. Your response to this question helps Sophia get a better sense of the pulse of crypto markets. And this ultimately translates into better insights for you when combined with Sophia's AI models. Your data empowers Sophia to provide you with even better intelligence going forward!

💣 When the Model Breaks

The 2026 shutdown wave is concentrated in projects that shared a common structural flaw: tokens designed to serve simultaneously as product utility, community incentive, and financing instrument. As CoinTelegraph's investigative feature documented, data compiled by analyst Stacy Muur shows that each month of 2026 saw at least one crypto project announce a shutdown. Decentralized email service Dmail announced its closure in April 2026 after high infrastructure costs, failed fundraising rounds, and weak token utility converged, with its token market cap having already fallen below USD 1 million in November 2025 per CoinGecko data. DAO tooling platform Tally, which provided software for managing decentralized governance processes, wound down after concluding that market had not developed at scale, while Step Finance shut down following a USD 40 million security breach in January 2026 after failing to secure either financing or an acquisition.

Roshan Dharia, restructuring advisor and CEO of crypto holding company Echo Base, identified the common thread: "Earlier cycles treated tokens as a primary funding mechanism with an implied alignment between users, holders and operators. That alignment has proven fragile in stressed scenarios, particularly where token holders lack defined rights or recourse." The failure mode is rarely a single catastrophic event. As Dharia noted, "You see this in cases like Tally and Step Finance, where there is no single failure point, just a steady decline in treasury value and user activity that compresses optionality over time."

On the question of recovery, Dharia was direct: "In prior cycles, projects could extend runway through new issuance or venture support. That path is largely closed, so losses are being recognized earlier, and outcomes are more often wind downs than recoveries." Venture deployment, as Dharia's characterization implies, has become more selective, and token issuance no longer reliably produces capital at the scale earlier cycles made possible.

⚖️ No Framework for Failure

Beyond the structural flaws in individual token models lies a systemic gap: crypto lacks a formal restructuring architecture comparable to what exists in traditional corporate distress. In conventional insolvency proceedings, creditor hierarchies, legal processes, and restructuring advisors create conditions for coordinated recovery. In crypto, those mechanisms are largely absent. Dharia described the consequence plainly: "Most projects do not have access to formal restructuring tools, and their stakeholder base is fragmented across token holders, equity investors, and users with no clear hierarchy or enforcement mechanism. That makes it difficult to recapitalize, restructure obligations, or run a controlled process to preserve value."

BlockFills illustrated the severity of this gap. The firm filed for bankruptcy in March 2026 after freezing withdrawals, with creditor Dominion Capital alleging that customer assets had been commingled to cover company losses. The absence of enforceable stakeholder rights did not merely complicate recovery; it accelerated the collapse by removing any structured path to value preservation. The pattern across these cases suggests that wind-down and distressed asset sales tend to be predictable outcomes of an architecture not designed for stress, rather than pure failures of execution.

The structural deficit matters more now because regulators are paying closer attention. A CertiK analysis of 2025 enforcement trends found that U.S. DOJ and FinCEN imposed USD 900 million in AML-related fines in the first half of 2025 alone, even as SEC crypto-specific penalties collapsed 97% year-over-year to USD 142 million. Projects operating with thin compliance infrastructure and fragmented governance now face regulatory exposure at the same moment their financing channels are closing.

🌐 The Regulatory Floor Is Rising

The compliance pressure is not limited to the United States. On April 28, 2026, Japan's Financial Services Agency and the National Police Agency, acting alongside two other government agencies, issued a joint guidance request to major real estate and crypto industry bodies demanding stricter AML controls on property transactions. The request stated that "crypto assets, which have the nature of being transferred instantly across national borders, are considered to pose a high risk of being used as a payment method in real estate transactions for the purpose of money laundering." Under Japan's Foreign Exchange and Foreign Trade Act, agents receiving crypto worth more than 30 million yen, approximately USD 180,000, from overseas are now required to file payment reports with regulators.

The guidance reflects a broader pattern of regulators building compliance floors beneath markets that had previously operated without them. For crypto projects, this creates a compounding pressure: weaker token utility, defined as a token's capacity to serve a genuine, auditable function within a real user economy rather than simply funding operations and rewarding early holders, reduces the financing runway, while rising compliance obligations increase the operational cost base. These two forces are not sequential; they bear down simultaneously on the same fragile treasury positions.

Analysts suggest that the sorting process underway in 2026 favors projects whose token models can demonstrate utility, stakeholder clarity, and compliance readiness under real operating conditions. Whether a sufficient number of existing projects meet that standard, and whether the industry develops formal restructuring tools before the next distress cycle, remains, at this stage, an open question.

Indicia Labs does not provide investment, tax, or legal advice. You are solely responsible for determining the suitability of any investment, investment strategy, or related transaction based on your personal investment objectives, financial circumstances, and risk tolerance. Indicia Labs may offer educational information about digital assets, which may include blog posts, articles, third-party content, news feeds, tutorials, and videos. This information does not constitute any form of advice, and you should not rely on it as such. Indicia Labs does not recommend buying, earning, selling, or holding any digital asset and will not be responsible for any decisions you make based on the provided information. Any content provided by Indicia Labs may contain errors, inaccuracies, or outdated information and should not be relied upon for making any investment decisions and Indicia Labs and its affiliates hold no responsibility for the accuracy of the provided information or content.

As with any asset, the value of digital assets can fluctuate, and there is a significant risk of losing money when buying, selling, holding, or investing in digital assets. Consult your financial advisor, legal or tax professional regarding your specific situation and financial condition, and carefully consider whether trading or holding digital assets is suitable for you.

Indicia Labs is not registered with the U.S. Securities and Exchange Commission and does not offer securities services in the United States or to U.S. persons. You acknowledge that digital assets are not subject to protections or insurance provided by the Federal Deposit Insurance Corporation or the Securities Investor Protection Corporation.