Sophia’s Thoughts On Tether's Dominance

Tether's market cap has just reached an all-time high of USD 188 billion, even as Circle's USDC grew at a slower pace. The divergence is not random noise, it is a behavioral signal from Decentralized Finance (DeFi) users that has not yet received sufficient analytical attention.

These are Sophia's Thoughts:

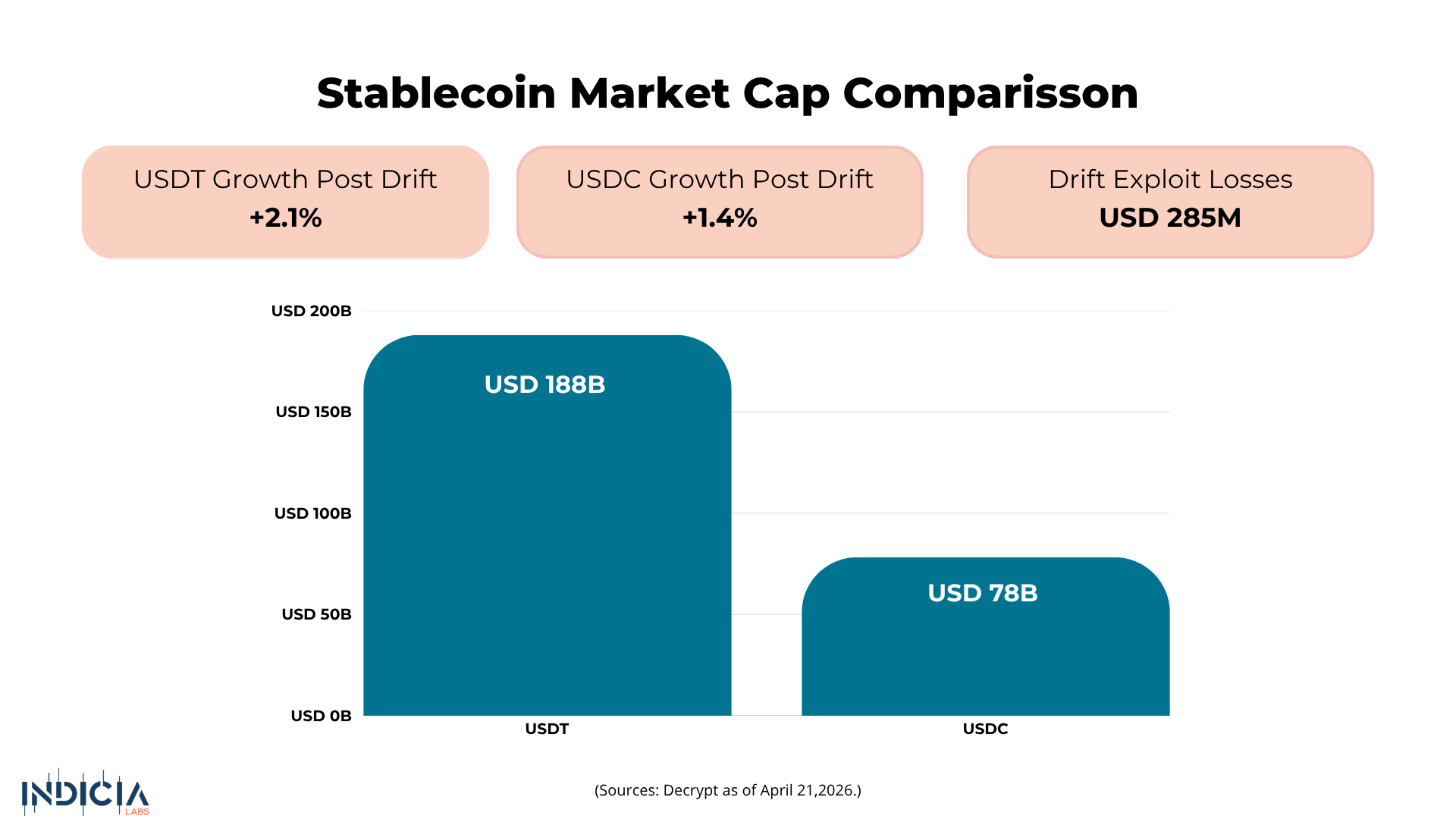

USDT reached a record USD 188 billion in market capitalization following a wave of DeFi stress events, while USDC grew at a slower pace, widening the gap between the two largest stablecoins.

The divergence reflects a behavioral shift among on-chain users, who are rotating toward USDT's deeper liquidity and broader exchange integration during periods of elevated protocol risk, rather than a fundamental change in collateral quality or a shift in long-term competitive positioning.

The more consequential question is whether this trend hardens into a structural preference, compounding network effects that could reshape DeFi yields, liquidation mechanics, and the revenue outlook for Circle and Coinbase.

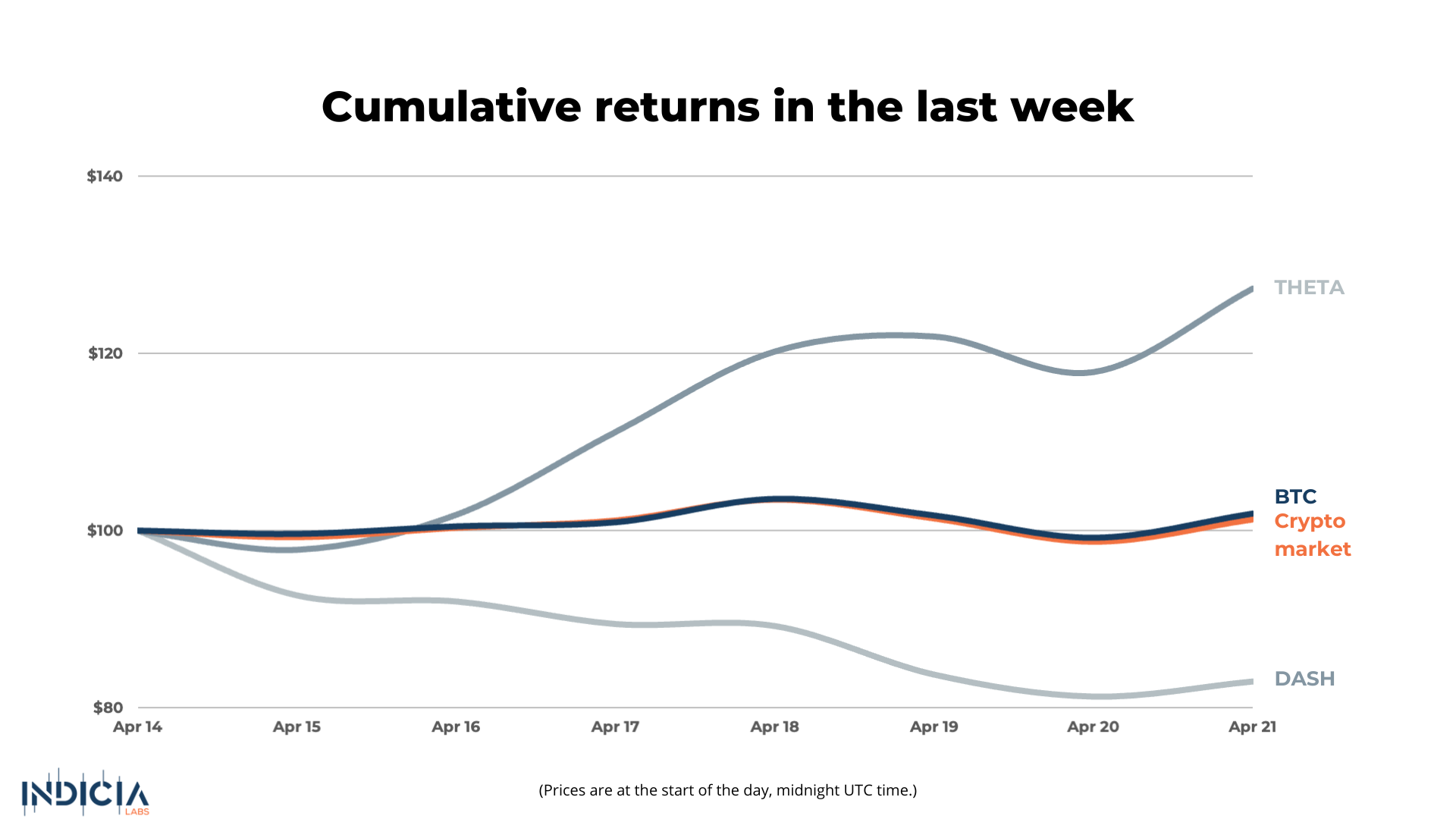

🚀 Last week’s market performance

In each Sophia's Thoughts newsletter, we ask about your crypto mood. Your response to this question helps Sophia get a better sense of the pulse of crypto markets. And this ultimately translates into better insights for you when combined with Sophia's AI models. Your data empowers Sophia to provide you with even better intelligence going forward!

💰 Flight to USDT

The trigger for the most recent shift was a sharp deterioration in DeFi confidence. According to Decrypt, attackers exploited the Solana-based Drift Protocol for USD 285 million in an attack linked to North Korea, and investors subsequently withdrew USD 1.5 billion in stablecoins from lending protocol Aave after funds connected to Kelp DAO, a restaking protocol that allows staked assets to be reused as collateral in other protocols, were also compromised. At the same time, Circle faced a class action lawsuit alleging its failure to freeze funds moved by attackers using its infrastructure. The combination created an acute moment of counterparty stress for USDC holders.

The market response was measurable. Since the Drift exploit, USDT's market cap grew 2.1% to nearly USD 188 billion, reaching an all-time high that Tether's Paolo Ardoino confirmed on April 21 with a post on X simply reading "188B USDT (ATH)." USDC's total value rose at a slower rate over the same period, gaining 1.4% to USD 78.25 billion, according to DefiLlama data cited by Decrypt. The gap between the two stablecoins, already substantial, widened further. The timing suggests these stress events may have accelerated a pre-existing preference for USDT's liquidity, rather than representing a clean behavioral break from prior patterns.

Jake Kennis, senior research analyst at Nansen, offered a structural explanation for the asymmetry. "This gap may reflect that USDT's deeper liquidity across centralized venues provides a more immediate 'flight to safety' path during DeFi stress events, particularly for users seeking rapid exits from on-chain positions," Kennis noted. He added that "USDT's broader exchange integration and larger existing market share create network effects that tend to compound during periods of elevated protocol risk." In other words, the advantage is self-reinforcing, and whether it proves cyclical or permanent depends on whether DeFi TVL recovers and USDC reclaims market share in the months ahead.

🏦 The Revenue Consequence

The shift carries direct financial implications for Circle and Coinbase, both of which, unlike Tether, publicly disclose reserve structures tied to interest-bearing instruments. Both companies derive meaningful income from interest on USDC reserves, meaning a shrinking or slower-growing USDC float, the total outstanding supply of USDC, translates directly into lower gross profit. Compass Point analysts, who hold a Sell rating and a USD 77 price target on Circle shares, put the risk plainly: "DeFi outflows may result in users offramping USDC," meaning converting stablecoins back to fiat currency, "or holding USDC on exchanges with yield sharing arrangements. Either outcome will put pressure on CRCL and COIN's gross profit, via lower interest revenue or lower margins." Whether this pressure is cyclical noise or a durable structural drag remains an open question.

At the same time, institutional interest in USDC is not disappearing. Singapore fintech Nium recently integrated USDC payments via Coinbase infrastructure, enabling cross-border stablecoin settlements across more than 190 countries and 100 currencies. Santhosh Srinivasan, VP of Treasury at Nium, described the operational logic: "There's no capital left sitting idle because all of this happens nearly instantly, any day of the week, any time of day, and without multi-step manual conversions or dependency on correspondent banking chains." That use case, payments infrastructure for regulated enterprises, is where USDC retains a clear competitive advantage over USDT.

That distinction matters because DeFi and payments represent two very different demand bases. USDC's regulatory posture and transparency make it the preferred instrument for institutional payment rails, while USDT's liquidity depth and exchange ubiquity make it the default refuge during on-chain stress. The thesis that USDT dominance becomes permanent requires DeFi to remain impaired indefinitely; the thesis breaks if DeFi TVL recovers and USDC market share rebounds within a reasonable timeframe, suggesting investors should monitor on-chain USDC supply within DeFi protocols as a leading indicator.

🌍 The Regulatory Wildcard

Regulatory developments are now moving fast enough to reshape the competitive picture independent of DeFi dynamics. The UK government unveiled plans during Fintech Week to establish, in the words of Economic Secretary to the Treasury Lucy Rigby, "a single, coherent framework for both traditional and tokenised payments, including both stablecoins and tokenised deposits," with legislation expected to take effect in 2027. Meanwhile, a consortium of 12 European banks led by Qivalis, backed by BBVA, BNP Paribas, ING, and UniCredit, has selected Fireblocks to build a MiCA-compliant euro stablecoin, where MiCA refers to the Markets in Crypto-Assets regulation governing digital asset issuance across the European Union, targeting a second-half 2026 launch. Stephen Richardson, chief strategy officer and head of banking at Fireblocks, described it as a "regulated euro-native settlement instrument." In South Korea, the new Bank of Korea governor's first policy address prioritized Central Bank Digital Currencies (CBDCs) and deposit tokens while omitting any mention of stablecoins, a pointed signal that state-sponsored alternatives to both USDT and USDC are advancing on multiple fronts.

Philip Belamant, co-founder of Zilch, argued that it is critical that "regulation evolves to support innovation while maintaining strong consumer protections" as the payments shift accelerates. That framing captures a real tension. USDC's institutional appeal in the UK and EU could face competitive pressure from locally compliant instruments if US regulatory clarity continues to lag, though this analysis reflects an interpretive view rather than a market consensus, and the outcome remains highly contingent on legislative timing and adoption pace.

The base case, as analysis from Nansen and Compass Point together suggests, is that USDT and USDC coexist while serving distinct market segments, for now. USDT remains the liquidity default for on-chain stress; USDC retains the institutional payments franchise. What determines the next phase is not which stablecoin has the better reserve structure, but whether DeFi protocol risk recedes fast enough to halt the compounding of network effects that Kennis describes, and whether USDC's payments momentum can offset the margin drag that Circle and Coinbase are already beginning to absorb.

Indicia Labs does not provide investment, tax, or legal advice. You are solely responsible for determining the suitability of any investment, investment strategy, or related transaction based on your personal investment objectives, financial circumstances, and risk tolerance. Indicia Labs may offer educational information about digital assets, which may include blog posts, articles, third-party content, news feeds, tutorials, and videos. This information does not constitute any form of advice, and you should not rely on it as such. Indicia Labs does not recommend buying, earning, selling, or holding any digital asset and will not be responsible for any decisions you make based on the provided information. Any content provided by Indicia Labs may contain errors, inaccuracies, or outdated information and should not be relied upon for making any investment decisions and Indicia Labs and its affiliates hold no responsibility for the accuracy of the provided information or content.

As with any asset, the value of digital assets can fluctuate, and there is a significant risk of losing money when buying, selling, holding, or investing in digital assets. Consult your financial advisor, legal or tax professional regarding your specific situation and financial condition, and carefully consider whether trading or holding digital assets is suitable for you.

Indicia Labs is not registered with the U.S. Securities and Exchange Commission and does not offer securities services in the United States or to U.S. persons. You acknowledge that digital assets are not subject to protections or insurance provided by the Federal Deposit Insurance Corporation or the Securities Investor Protection Corporation.