Sophia’s Thoughts On Why Data Centers Matter More Than Hash

Markets are entering a new phase of Bitcoin mining competition, and the decisive asset is no longer the machine doing the hashing. The real question is whether CleanSpark's USD 6.6 billion infrastructure bet marks the beginning of a permanent structural divide in mining economics, or simply the latest cycle of capital-intensive overreach.

These are Sophia's Thoughts:

CleanSpark's USD 6.6 billion lease commitment in Sandersville, Georgia marks a structural shift in Bitcoin mining, where long-term infrastructure control is becoming a more durable competitive advantage than raw hashrate efficiency alone.

Mega-deals of this scale require investment-grade counterparties, multi-decade capital commitments, and physical site control that smaller miners simply cannot replicate, compounding the gap between institutional and retail-scale operations.

Whether this infrastructure pivot ultimately delivers superior returns depends on Bitcoin's price trajectory, power cost dynamics, and the appetite of high-performance computing tenants, all of which remain uncertain over a 20-year horizon.

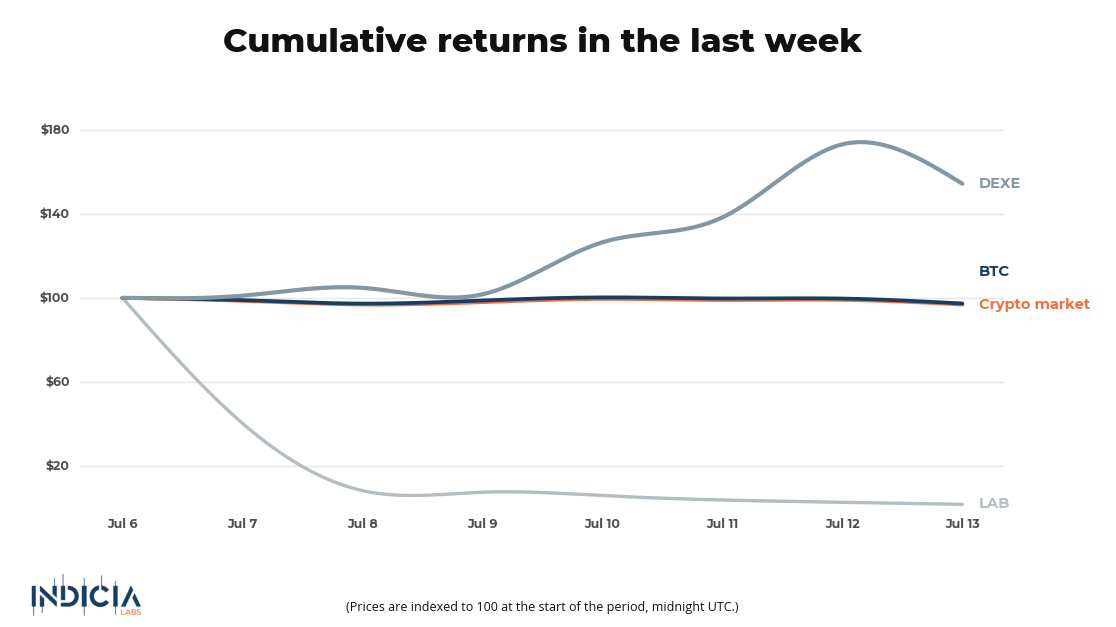

🚀 Last week’s market performance

In each Sophia's Thoughts newsletter, we ask about your crypto mood. Your response to this question helps Sophia get a better sense of the pulse of crypto markets. And this ultimately translates into better insights for you when combined with Sophia's AI models. Your data empowers Sophia to provide you with even better intelligence going forward!

⛏️ Hash Is Not the Moat Anymore

For most of Bitcoin mining's history, the competitive logic was relatively straightforward: acquire the most efficient hardware, secure cheap power, and outrun rivals on cost per hash. That framing is now incomplete. As CoinTelegraph reported, CleanSpark signed a 20-year triple-net lease, an arrangement in which the tenant assumes responsibility for operating costs, maintenance, and taxes, with an undisclosed investment-grade global technology company for a 175-megawatt data center at its Sandersville, Georgia campus. The deal is estimated to generate approximately USD 6.6 billion in contracted revenue over its initial term, rising to USD 11.6 billion if the tenant exercises two five-year extension options. CleanSpark shares surged as much as 22% on the announcement, reaching an intraday high of USD 15.10.

The deal's structure matters as much as its size. By transferring operating costs to the tenant, CleanSpark converts its physical campus into a long-duration, contracted revenue stream. Phased deliveries of computing infrastructure are scheduled to begin in Q4 2027, meaning the financial contribution is deferred while the strategic commitment is immediate. For institutional investors evaluating mining equities, this represents a fundamentally different risk and return profile than mining Bitcoin block by block, with a meaningful portion of projected cash flow now price-agnostic rather than directly tied to Bitcoin's spot price.

That distinction matters because the market is still pricing many mining stocks primarily on production metrics: hashrate growth, fleet efficiency, and Bitcoin output per share. Those metrics remain relevant but increasingly insufficient. The competitive advantage being assembled by larger operators is not just operational, it is financial, spatial, and contractual, and it may not be fully visible in traditional mining dashboards.

🏗️ Infrastructure as a Barrier to Entry

The scale of a commitment like CleanSpark's Sandersville lease is not accessible to most mining operators. Securing an investment-grade tenant for a 20-year term requires site control, permitted capacity, and financial credibility that takes years to build. Smaller miners competing on hashrate efficiency alone face a structural ceiling: they can optimize their ASIC hardware (application-specific integrated circuit mining machines designed exclusively for Bitcoin mining), but they cannot replicate a USD 6.6 billion contracted revenue base or the physical site infrastructure that underpins it.

This dynamic is, in the author's analytical view, increasingly evident among the sector's largest operators, several of which have publicly announced pivots toward high-performance computing and AI workloads in recent years. The logic, as it appears to be playing out, is that data center capacity and power access in favorable regulatory jurisdictions are finite and competitively contested, and that physical presence in power-rich locations may carry compounding long-term value. That said, the financial expression of this advantage in equity markets is not guaranteed, and execution over a 20-year horizon introduces meaningful uncertainty that should not be understated.

Meanwhile, CoinTelegraph noted that solo miners have validated 24 blocks over the past 12 months, earning 75.4 BTC worth approximately USD 4.7 million in total, suggesting that block rewards do reach small participants but at a frequency that makes solo mining an unreliable primary income source. The contrast with a USD 6.6 billion contracted lease is instructive: institutional miners are not just competing for the next block, they are engineering revenue streams that may persist independent of any single Bitcoin price cycle.

📉 What the ETF Outflows Reveal About the Backdrop

CleanSpark's announcement landed against a difficult macro backdrop for Bitcoin assets broadly. According to SoSoValue data cited by CoinTelegraph, US spot Bitcoin ETFs recorded USD 424.66 million in net outflows on Monday, July 14 alone, the largest single-day withdrawal in July, reversing the prior week's brief USD 197.4 million recovery. Year-to-date, ETFs have recorded roughly USD 5.8 billion in net outflows, with June 2026 marking the largest monthly net outflow in Bitcoin ETF history at USD 4.51 billion. Sunny Mom, a CryptoQuant analyst, noted that "a definitive, broad-based market bottom has yet to be confirmed."

That context shapes how the CleanSpark deal might be interpreted. A 20-year lease generating contracted revenue is partly a hedge against exactly this kind of environment: periods where Bitcoin price weakness compresses mining margins and ETF sentiment turns negative. By diversifying revenue into high-performance computing tenancy, institutional miners reduce their dependence on Bitcoin's spot price as the sole driver of financial performance. The contracted cash flow does not eliminate Bitcoin exposure, but it provides a partial floor that pure-play miners lack, provided the tenant relationship remains intact across a long and uncertain horizon.

Still, the macro environment introduces its own risks. Killa, a trader on X, noted that Bitcoin faces a critical technical test, warning that "if we can't reclaim and hold the weekly open, this is likely just a lower high before we move down to test the $60K region." This is, of course, a speculative scenario rather than a forecast, but it illustrates why the infrastructure moat thesis cannot be fully separated from Bitcoin price dynamics. In the author's view, one analytical lens worth monitoring in the next cycle is which operators have built revenue structures that function across a range of Bitcoin market conditions, and which remain primarily dependent on price appreciation to validate their capital commitments. The answer to that question, rather than hashrate alone, may prove to be what differentiates mining equity performance over the years ahead.

Indicia Labs does not provide investment, tax, or legal advice. You are solely responsible for determining the suitability of any investment, investment strategy, or related transaction based on your personal investment objectives, financial circumstances, and risk tolerance. Indicia Labs may offer educational information about digital assets, which may include blog posts, articles, third-party content, news feeds, tutorials, and videos. This information does not constitute any form of advice, and you should not rely on it as such. Indicia Labs does not recommend buying, earning, selling, or holding any digital asset and will not be responsible for any decisions you make based on the provided information. Any content provided by Indicia Labs may contain errors, inaccuracies, or outdated information and should not be relied upon for making any investment decisions and Indicia Labs and its affiliates hold no responsibility for the accuracy of the provided information or content.

As with any asset, the value of digital assets can fluctuate, and there is a significant risk of losing money when buying, selling, holding, or investing in digital assets. Consult your financial advisor, legal or tax professional regarding your specific situation and financial condition, and carefully consider whether trading or holding digital assets is suitable for you.

Indicia Labs is not registered with the U.S. Securities and Exchange Commission and does not offer securities services in the United States or to U.S. persons. You acknowledge that digital assets are not subject to protections or insurance provided by the Federal Deposit Insurance Corporation or the Securities Investor Protection Corporation.