Sophia’s Thoughts On RWA Tokenization Reaching Escape Velocity

Tokenized real-world assets have reached USD 51 billion by at least one major estimate, though figures vary materially depending on methodology. The question is whether the institutional capital now arriving represents a durable structural shift or a tide that regulatory friction could quickly reverse.

These are Sophia's Thoughts:

Bernstein Research data show the tokenized RWA market has reached USD 51 billion, up 42% year-to-date, with private credit accounting for roughly 44% of total value as yield-seeking capital meets settlement infrastructure built directly on blockchain networks rather than adapted from legacy financial systems.

Major institutions including BlackRock and Franklin Templeton have committed real capital to tokenization, but the ecosystem remains fragmented across chains and analytics providers, with headline figures ranging from USD 34 billion to USD 51 billion depending on what each provider counts as tokenized.

The trajectory hinges on whether regulatory frameworks in the United States can resolve outstanding tax and compliance burdens before jurisdictions with cleaner rulebooks capture the structural flows that are now clearly in motion.

🚀 Last week’s market performance

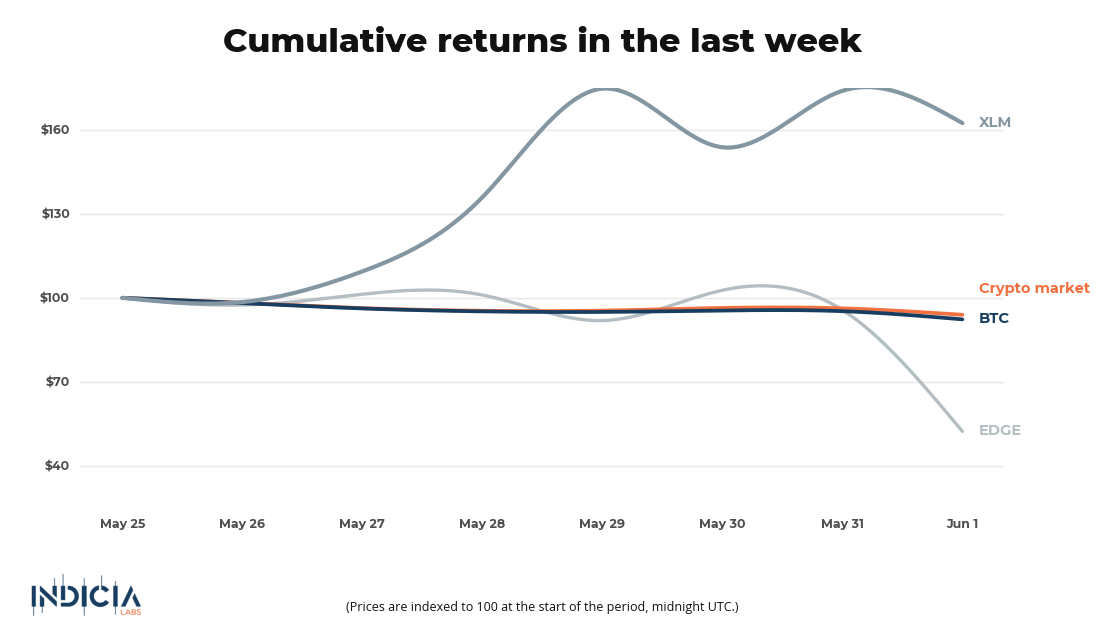

The broader crypto market gained 0.6% this week, with Bitcoin (BTC) up 0.5% as markets traded in a narrow range. NEAR Protocol (NEAR) was the standout performer, surging 70.5%, with market commentary pointing to momentum around the network's AI integration narrative. Chiliz (CHZ) was the week's worst performer, declining 24.1% as sentiment across the sports and entertainment token segment softened.

🧐 What is your crypto mood today?

In each Sophia's Thoughts newsletter, we ask about your crypto mood. Your response to this question helps Sophia get a better sense of the pulse of crypto markets. And this ultimately translates into better insights for you when combined with Sophia's AI models. Your data empowers Sophia to provide you with even better intelligence going forward!

📐 The Architecture of a USD 51 Billion Market

The tokenized RWA market has arrived at a figure that commands institutional attention. According to Bernstein Research, total tokenized RWA value reached USD 51 billion as of May 2026, with Figure Technology Solutions (an on-chain lending platform) ranked first among platforms at USD 18 billion in assets. BlackRock's tokenized money market fund BUIDL has surpassed USD 2.5 billion on its own. Private credit, at roughly 44% of total market value, now leads all segments.

The demand logic is straightforward. As Ross Shemeliak, co-founder of Stobox, put it: "Private credit is becoming one of the fastest-growing sectors in real-world assets because it solves two major problems at once: investors want yield, and businesses need capital." On-chain settlement compresses the operational friction that has historically made private credit inaccessible at scale. As cited by CoinTelegraph, Boston Consulting Group observed that "digital assets are increasingly shifting beyond speculative trading toward infrastructure tied to payments, settlement and capital markets."

Still, a methodological gap deserves acknowledgment. RWA.xyz pegs the market at USD 34 billion, a figure materially lower than Bernstein's estimate, reflecting differences in what each provider counts as tokenized, including whether custodial assets, chain-hopped positions, or re-tokenized instruments are included. That discrepancy matters because inflated headline numbers have historically preceded sharp narrative corrections in crypto. The structural outlook, from a market-development perspective, appears constructive, but the range of estimates signals that market-wide data standards have not yet caught up with market-wide growth.

🏛️ Institutional Conviction, Measured

The clearest signal of durability is that the institutions entering RWA tokenization are not doing so tentatively. Franklin Templeton, one of the world's largest asset managers, moved its tokenization infrastructure from the Stellar blockchain to Canton, a transition documented by Decrypt in January 2026 that reflects the operational seriousness behind the commitment. BlackRock CEO Larry Fink, in reporting from January 2026, publicly advocated for a single blockchain for tokenization to avoid corruption and aid in scaling, according to Decrypt. PwC, in the same January 2026 reporting, stated that "crypto adoption is no longer reversible."

Recent product-level activity reinforces the picture. Grvt and Plume are launching three tokenized RWA yield products, including the Base Yield Fund, Balanced Fund, and Opportunistic Fund, with one product tied to the iShares AAA CLO (Collateralized Loan Obligation, a security backed by a pool of business loans) Active ETF, which holds USD 2.2 billion in assets. Meanwhile, the XRP Ledger, which already holds over USD 3 billion in tokenized RWAs onchain, is considering a draft amendment that would add concentrated liquidity and StableSwap curves (curve types that allow liquidity providers to concentrate capital within specific price ranges, improving capital efficiency) to its automated market maker, as reported by CoinDesk. Improved capital efficiency on settlement-focused chains could meaningfully reduce the cost of holding tokenized positions.

That said, product launches and capital commitment are distinct signals. Shemeliak's framing captures the longer arc: "The bigger story is not whether private credit is number one today. The real story is that blockchain is quietly becoming the infrastructure layer for global capital markets." Whether that proves correct depends less on product launches and more on the regulatory conditions under which those products can operate, and on whether the AUM figures attached to early platforms reflect durable reallocation or exploratory positioning.

⚖️ The Regulatory Fault Line

Institutional conviction and regulatory friction are not mutually exclusive forces, and the U.S. market is testing both simultaneously. The Clarity Act is designed to provide enforceable guardrails, moving the industry away from the regulation-by-enforcement posture of recent years. But, as Robin Singh argued in a CoinDesk opinion piece, "regulatory clarity does not automatically lead to adoption. Because even if Congress gets the market structure right, the U.S. crypto tax framework, in its current form, is still a bit messy and complicated."

The compliance burden is specific and operational. Form 1099-DA, the IRS's new digital asset reporting form, requires disclosure of acquisition dates, disposal dates, and asset counts, but when assets move between platforms, the cost basis often disappears entirely. Singh noted that "crypto users are now receiving tax forms that often report proceeds without a reliable cost basis, fail to properly capture holding periods and excludes [sic] non-custodial activity entirely." For RWA platforms that involve layered asset movement across chains, custodians, and settlement venues, institutional legal teams will price that audit exposure conservatively, creating a structural drag on deployment decisions rather than a recoverable inconvenience.

The jurisdictional competition is already visible. Bermuda has amended its legislation to accept digital assets for public taxes and is partnering with Circle, Coinbase, and Stellar to build what it describes as the world's first fully onchain economy. Craig Swan of the Bermuda Monetary Authority acknowledged that legislation around smart contracts and share registers still requires clarification, but the direction of travel is unambiguous. Singh's warning carries structural weight: "The U.S. won't need to ban crypto to slow its growth, but it may tax it into friction, while other jurisdictions design systems that make participation materially easier." If that divergence widens, the USD 51 billion figure may continue to grow globally even as U.S.-domiciled capital faces structural headwinds that redirect flows toward more accommodating regulatory environments, with traditional finance remaining a viable alternative for allocators unwilling to absorb either the friction or the jurisdictional uncertainty.

Indicia Labs does not provide investment, tax, or legal advice. You are solely responsible for determining the suitability of any investment, investment strategy, or related transaction based on your personal investment objectives, financial circumstances, and risk tolerance. Indicia Labs may offer educational information about digital assets, which may include blog posts, articles, third-party content, news feeds, tutorials, and videos. This information does not constitute any form of advice, and you should not rely on it as such. Indicia Labs does not recommend buying, earning, selling, or holding any digital asset and will not be responsible for any decisions you make based on the provided information. Any content provided by Indicia Labs may contain errors, inaccuracies, or outdated information and should not be relied upon for making any investment decisions and Indicia Labs and its affiliates hold no responsibility for the accuracy of the provided information or content.

As with any asset, the value of digital assets can fluctuate, and there is a significant risk of losing money when buying, selling, holding, or investing in digital assets. Consult your financial advisor, legal or tax professional regarding your specific situation and financial condition, and carefully consider whether trading or holding digital assets is suitable for you.

Indicia Labs is not registered with the U.S. Securities and Exchange Commission and does not offer securities services in the United States or to U.S. persons. You acknowledge that digital assets are not subject to protections or insurance provided by the Federal Deposit Insurance Corporation or the Securities Investor Protection Corporation.