Sophia’s Thoughts On Stablecoin Wars

The stablecoin market is fracturing along a new fault line. More than 140 companies, including Coinbase, BlackRock, Visa, Mastercard, and American Express, have coalesced behind Open USD, and the question markets are now asking is whether Circle can hold its ground.

These are Sophia's Thoughts:

The launch of Open USD (OUSD), backed by more than 140 institutional names, sent Circle's stock down nearly 16% in a single session and raises serious structural questions about USDC's long-term market position.

The consortium model is not simply a new stablecoin; it represents a coordinated effort to shift stablecoin infrastructure away from issuer-controlled models toward open, low-cost, business-aligned rails that could reorder the competitive hierarchy.

With business adoption accelerating and rival products multiplying, the decisive factor will not be which stablecoin launches with the most backers; it will be which one earns and holds institutional trust at scale.

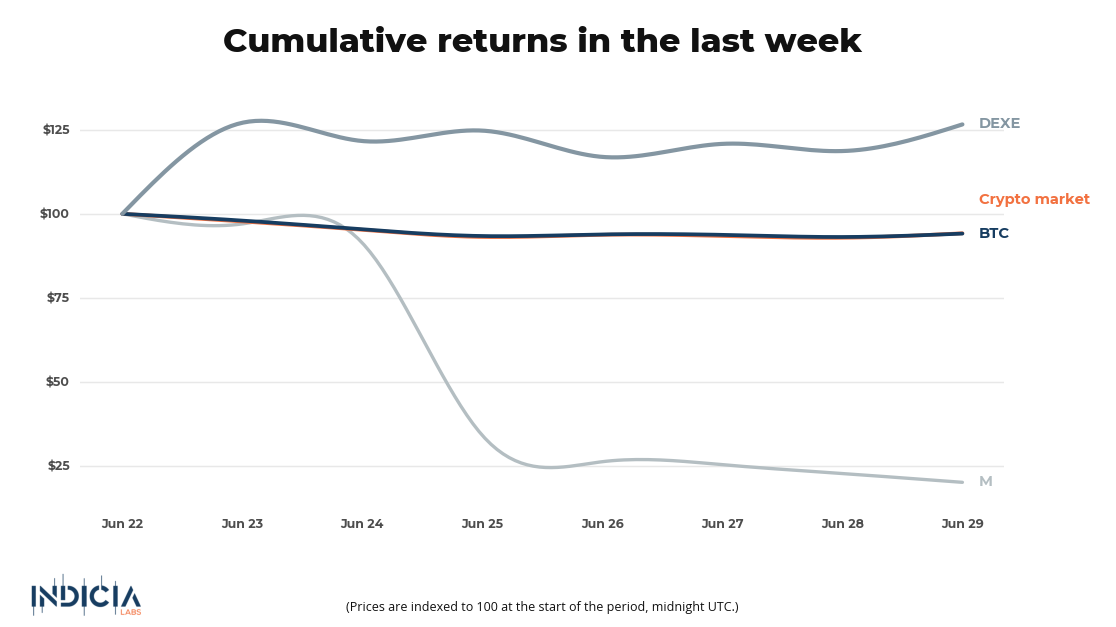

🚀 Last week’s market performance

The crypto market fell 5.8% this week, with Bitcoin (BTC) declining 5.9% as risk-off sentiment weighed broadly on digital assets. DEXE (DEXE) was the week's standout performer, gaining 26.6%, though the specific catalyst for its move had not been confirmed at time of writing. The worst performer was M (M), which shed 79.9% as sentiment around the project collapsed sharply.

🧐 What is your crypto mood today?

In each Sophia's Thoughts newsletter, we ask about your crypto mood. Your response to this question helps Sophia get a better sense of the pulse of crypto markets. And this ultimately translates into better insights for you when combined with Sophia's AI models. Your data empowers Sophia to provide you with even better intelligence going forward!

⚔️ The Consortium Arrives

The stablecoin market has received a significant structural challenge. As Decrypt reported, more than 140 companies have coalesced around Open USD (OUSD), an independent entity called Open Standard that promises free minting and redemption with no volume caps. OUSD is expected to go live later in 2026. Circle's stock fell nearly 16% on the day of the announcement to USD 63.99, and had declined approximately 39% over the prior month. Whether the single-day move reflected the OUSD announcement alone or a combination of macro factors and rotation dynamics is difficult to isolate, though the timing was unambiguous.

Zach Abrams, founding CEO of Open Standard, who previously founded Bridge, a stablecoin company acquired by Stripe, framed the proposition in direct terms: "Existing stablecoins have great strengths, but to use them at scale, businesses need something that's open, low-cost, high-throughput, broadly accessible, and aligned to their interests." Samara Cohen of BlackRock described the initiative as "a constructive step toward giving businesses more choice." The language from both suggests a deliberate positioning against the fee structures and gatekeeping that have characterized existing issuer-controlled stablecoins.

That distinction matters because USDC's commercial model depends on interest income from reserves and, increasingly, revenue-sharing arrangements with distribution partners. A consortium stablecoin designed around zero minting costs does not merely compete on price; it restructures the incentive architecture of the entire market. Whether Open Standard can execute on that promise at institutional scale, and how it resolves reserve yield allocation and regulatory accountability across 140 backing entities, remains an open question. Distribution is a genuine advantage for OUSD, given the depth of its founding consortium, though operational coordination at that scale introduces execution risks that are not yet visible.

🏛️ Circle's Institutional Moat

Circle's position is not without substance. As CoinTelegraph reported, BNY has expanded its Digital Asset Custody platform to allow institutional clients to store, transfer, mint, and redeem USDC, making it the first stablecoin supported on that platform. BNY oversees USD 59.3 trillion in assets under custody and administration and serves more than 90% of Fortune 100 companies. USDC currently circulates at more than USD 73.8 billion, according to DefiLlama data, and BNY serves as its primary reserve custodian.

That relationship matters for reasons that go beyond brand association. Institutional adoption of any financial instrument is partly a function of custody infrastructure, compliance integration, and counterparty risk. Migrating from USDC to a new stablecoin would require custody re-engineering, compliance recertification, and operational testing, all of which carry measurable time and capital costs. Open USD may offer lower costs at the minting layer, but the integration friction embedded in the USDC-BNY relationship will not be immediately resolved, regardless of how many companies sign the founding consortium.

ARK Invest's activity during the selloff is also notable as a market data point. As CoinTelegraph reported, ARK added approximately 169,777 shares in Circle worth roughly USD 12.9 million over three trading days ending June 30, even as the stock declined. At the same time, ARK added USD 18.6 million in Coinbase shares, with Coinbase being one of OUSD's core backers. These purchases reflect ARK's own institutional strategy and should not be read as a directional signal; however, the fact that the firm added to both sides of this competitive divide suggests it may view the stablecoin market as one where multiple players could coexist rather than a single-issuer winner-takes-most outcome.

🌐 Adoption Is Already Structural

The competition over stablecoin infrastructure is not theoretical. Business adoption data points to a market that has already crossed an inflection point. According to a Cybrid report covered by CoinTelegraph, 42% of businesses surveyed are already using stablecoins for cross-border payments, with 88% saying they are likely or very likely to do so within the next 12 months. Only 2% of respondents identified as committed users of traditional payment rails, and companies processing more than USD 100 million in monthly payment volume reported average savings of up to 47%.

That commercial context explains why the product competition is intensifying on multiple fronts simultaneously. Investment firm Spiko has integrated Coinbase Payments into two EU-regulated UCITS Treasury-bill funds, with UCITS being the European Union's framework for regulated collective investment funds, with transactions settling on Base, Coinbase's layer-2 network, a faster, lower-cost blockchain built on top of Ethereum, as CoinTelegraph reported. Coinbase described these as the first UCITS funds in Europe to accept direct stablecoin payments. Meanwhile, MetaMask launched its Money Account product, which offers up to 4% variable APY on its mUSD stablecoin through decentralized lending protocols, software-based platforms that allow users to borrow and lend assets without a traditional financial intermediary, including Aave and Morpho. Johann Bornman, MetaMask's Senior Director of Product, described the yield structure plainly: "Bridge holds the reserves (U.S. dollars and short-term Treasury bills) that back mUSD 1:1. When users deposit into Money Account, those funds are deployed via Veda's vault infrastructure into established DeFi lending protocols like Aave and Morpho." The full product details are covered by both CoinTelegraph and Decrypt.

The aggregate picture is one where multiple well-capitalized players are converging on stablecoin infrastructure from different directions simultaneously. USDC faces pressure from above, in the form of the OUSD consortium, and from below, as yield-bearing alternatives like mUSD compete for user deposits. The central question is not whether Circle faces a credible competitive threat; it does. The question is whether the stablecoin market resolves into a winner-takes-most structure or stratifies by use case, with USDC retaining the institutional custody layer while newer entrants capture cost-sensitive commercial and retail segments. The metrics worth monitoring in the months ahead include USDC's on-chain settlement volume relative to overall stablecoin flow, the pace of BNY client adoption, and whether OUSD can demonstrate regulatory clarity on reserve accountability before its expected 2026 launch.

Indicia Labs does not provide investment, tax, or legal advice. You are solely responsible for determining the suitability of any investment, investment strategy, or related transaction based on your personal investment objectives, financial circumstances, and risk tolerance. Indicia Labs may offer educational information about digital assets, which may include blog posts, articles, third-party content, news feeds, tutorials, and videos. This information does not constitute any form of advice, and you should not rely on it as such. Indicia Labs does not recommend buying, earning, selling, or holding any digital asset and will not be responsible for any decisions you make based on the provided information. Any content provided by Indicia Labs may contain errors, inaccuracies, or outdated information and should not be relied upon for making any investment decisions and Indicia Labs and its affiliates hold no responsibility for the accuracy of the provided information or content.

As with any asset, the value of digital assets can fluctuate, and there is a significant risk of losing money when buying, selling, holding, or investing in digital assets. Consult your financial advisor, legal or tax professional regarding your specific situation and financial condition, and carefully consider whether trading or holding digital assets is suitable for you.

Indicia Labs is not registered with the U.S. Securities and Exchange Commission and does not offer securities services in the United States or to U.S. persons. You acknowledge that digital assets are not subject to protections or insurance provided by the Federal Deposit Insurance Corporation or the Securities Investor Protection Corporation.